SSDI vs. SSI vs. SSA: What’s the Difference?

Introduction

Many people researching disability benefits are trying to answer practical questions:

What does SSA actually mean?

What is the difference between SSDI and SSI?

Can retirement benefits affect disability payments?

Can someone qualify for more than one program at the same time?

Part of the confusion comes from how closely these programs are connected. SSDI, SSI, and Social Security retirement benefits are all administered through the Social Security Administration, but each program follows different rules involving work history, medical eligibility, income limits, and age.

Understanding the differences can make it easier to start disability paperwork, organize financial records, and know which type of benefit may apply to your situation.

The short explanation looks like this:

SSA is the agency.

SSDI is disability insurance based on work history.

SSI is a needs-based assistance program.

Social Security retirement benefits are based on age and work history.

Once these programs are separated clearly, the system often becomes easier to understand.

What Is SSA?

SSA stands for the Social Security Administration, the federal agency that manages several major benefit programs in the United States. The Social Security Administration oversees:

Social Security retirement benefits

Social Security Disability Insurance (SSDI)

Supplemental Security Income (SSI)

Survivor benefits

Medicare enrollment functions

Social Security earnings records and Social Security numbers

In simple terms, SSA is the organization that runs the programs. It is not a monthly benefit itself.

You can think of SSA as the “umbrella agency,” while SSDI, SSI, and retirement benefits are separate programs managed underneath it.

Where are the SSA Rules and Regulations?

The SSA operates under the federal Social Security Act and follows regulations published primarily in Title 20 of the Code of Federal Regulations (CFR). Although SSA manages several different programs, each program follows somewhat different eligibility rules and regulations. Retirement benefits are generally governed by age, earnings history, and insured status rules, while SSDI focuses heavily on disability standards and work credits. SSI, by comparison, uses financial-need rules involving income, resources, and living arrangements. (You can find links to Title 20 in the References section at the end of this article.)

What Is SSDI?

Social Security Disability Insurance Explained

Social Security Disability Insurance (SSDI) is a federal disability insurance program for workers who have paid Social Security taxes through employment.

Workers contribute to the Social Security system through payroll taxes deducted from their paychecks. Those contributions may create “insured status” for SSDI purposes if the worker later develops a qualifying medical condition.

To qualify for SSDI, applicants generally must meet both work-credit requirements and SSA’s federal definition of disability. In most cases, the medical condition must be expected to last at least 12 months or result in death, prevent substantial gainful activity, and be supported by medical evidence.

Under SSA regulations, disability claims are usually evaluated through a five-step sequential evaluation process that reviews current work activity, severity of medical conditions, past work, residual functional capacity, and the ability to adjust to other work.

During this review, SSA may examine medical evidence:

Medical records

Treatment history

Physician opinions

Functional limitations

Duration of the condition

Work-related limitations

Where These SSDI Rules Come From

SSDI is primarily governed by Title II of the Social Security Act and regulations found mainly in Part 404 of Title 20 of the Code of Federal Regulations (20 CFR Part 404). One of the most important sections for disability applicants is Subpart P of Part 404, which also contains the medical-vocational disability evaluation rules SSA uses to determine whether a person meets the federal definition of disability. Subpart P includes the Listing of Impairments, commonly called the “Blue Book,” along with the medical-vocational guidelines known as the grid rules. If you look at Part 404 (Title 20) in the electronic Code of Federal Regulations (eCFR), you’ll see Appendix 1 in Subpart P includes the Listing of Impairments, and Appendix 2 in Subpart P includes the Medical and Vocational guidelines. (You can read the startdisability.com articles on Rules and Regulations to learn more about SSDI regulations. You can also review the References section at the end of this article for links to these specific SSDI regulations and the eCFR.)

In some situations, SSA applies the “grid rules,” particularly for older workers approaching retirement age. Some severe medical conditions may also qualify for expedited review through the Compassionate Allowance program.

Key Features of SSDI

Work Credits Matter

SSDI is tied closely to employment history. Applicants generally need enough recent work credits earned through jobs covered by Social Security taxes.

The number of required work credits depends partly on age and work history.

SSDI Can Include Family Benefits

Certain spouses and children may qualify for benefits based on a disabled worker’s earnings record.

Medicare Eligibility

Many SSDI recipients become eligible for Medicare after a qualifying waiting period established under federal law. People who want to review the official Medicare waiting-period rules can visit the Social Security Administration’s Medicare information page at https://www.ssa.gov/disabilityresearch/wi/medicare.htm or the Medicare eligibility page at https://www.medicare.gov/basics/get-started-with-medicare. (These links are subject to change with government updates.)

What Is SSI?

Supplemental Security Income Explained

Supplemental Security Income (SSI) is different from SSDI because it is based primarily on financial need rather than work history.

SSI helps qualifying individuals who are:

Disabled

Blind

Age 65 or older

…and who have limited income and limited resources.

Unlike SSDI, SSI is funded through general federal tax revenues rather than Social Security payroll taxes.

Where can I find SSI rules and regulations?

SSI rules are primarily governed by Title XVI of the Social Security Act and regulations found mainly in Part 416 of Title 20 of the Code of Federal Regulations (20 CFR Part 416). These SSI-specific regulations explain how SSA evaluates countable income, resource limits, living arrangements, deeming of income from spouses or parents, disability eligibility, overpayments, and monthly payment calculations for SSI applicants and recipients. (You can find links to these SSI rules and regulations in the References section at the end of this article.)

Key Features of SSI

Work History Is Not Required

A person may qualify for SSI even if they have little or no prior work history.

This can include:

Adults with limited employment history

Children with qualifying disabilities

Individuals who became disabled early in life

Income and Asset Limits Apply

When determining financial eligibility for SSI, SSA reviews:

Household income

Financial resources

Living arrangements

Certain support received from others

Bank accounts, cash resources, and some property can affect SSI eligibility.

SSA also publishes detailed SSI financial eligibility information at https://www.ssa.gov/ssi/text-eligibility-ussi.htm.

Medicaid Eligibility

In many states, SSI recipients may also qualify for Medicaid coverage automatically or through a related process. Medicaid is generally a needs-based health coverage program tied closely to financial eligibility rules used in SSI.

This differs from SSDI, where eligible beneficiaries often qualify for Medicare instead, after a federal waiting period tied to disability entitlement rules. Medicare is a federal insurance program more closely connected to work history, payroll tax contributions, disability entitlement, or retirement eligibility rather than financial need.

SSI Payments Can Be Smaller Than SSDI

Because SSI is a needs-based program with federally established payment limits, monthly SSI payments are often smaller than SSDI benefits, which are generally based on a worker’s earnings history and prior payroll tax contributions. Some states also provide additional SSI state supplements.

What Are Social Security Retirement Benefits?

Social Security retirement benefits are monthly payments available to eligible workers who reach retirement age and have earned enough work credits during their careers.

Like SSDI, retirement benefits are generally based on prior earnings and payroll tax contributions.

The amount a person receives can depend on:

Lifetime earnings history

Age when benefits begin

Years worked

Social Security taxable earnings

What rules and regulations cover SSA retirement benefits?

Social Security retirement benefits are primarily governed by Title II of the Social Security Act and regulations found mainly in Part 404 of Title 20 of the Code of Federal Regulations (20 CFR Part 404). These retirement-specific regulations explain how SSA evaluates insured status, retirement age eligibility, earnings records, delayed retirement credits, early retirement reductions, spousal benefits, survivor benefits, and monthly retirement payment calculations.

Applicants researching retirement regulations often review sections involving Full Retirement Age (FRA), reduced early retirement benefits, delayed retirement credits, earnings limits before FRA, and family benefits payable on a worker’s earnings record.

Full Retirement Age Matters

The SSA uses a Full Retirement Age (FRA) system. Depending on birth year, FRA may range from age 66 to 67 for many current applicants.

People may begin retirement benefits earlier than FRA, but early retirement can reduce monthly payments.

Delaying retirement benefits beyond FRA may increase monthly payments in some situations.

Retirement Benefits Are Different From SSI and SSDI

Although all three programs are administered by SSA, retirement benefits follow different eligibility rules and regulations than SSI and SSDI. Social Security retirement benefits are primarily age-based and focus on a worker’s earnings history, insured status, and retirement age under Title II regulations in 20 CFR Part 404.

SSDI also falls under Title II and Part 404, but SSDI regulations focus heavily on disability eligibility, work limitations, and medical-vocational rules found in Subpart P. SSI, by contrast, is governed mainly by Title XVI and 20 CFR Part 416, which emphasize financial need, income limits, resource limits, and living arrangements.

Because SSI is needs-based, Social Security retirement income can sometimes reduce SSI payments or affect SSI eligibility entirely. People who take reduced early retirement benefits may also apply for SSDI at the same time in some situations, particularly if a serious medical condition prevents continued work before Full Retirement Age. SSDI can also affect retirement benefits because SSDI payments generally convert automatically into Social Security retirement benefits once a person reaches Full Retirement Age under SSA Title II regulations.

Why People Often Say “I Get SSA”

In everyday conversations, many people say they “get SSA” when they are actually referring to Social Security retirement benefits, early retirement, SSDI, or SSI. This informal language can create confusion because SSA is the federal agency, not the specific benefit program.

That confusion becomes especially important when someone is considering early retirement while also applying for SSDI, since the programs follow different eligibility and payment rules.

Can Someone Receive SSDI and Social Security Retirement Benefits at the Same Time?

This is one of the most misunderstood areas of Social Security benefits.

In most situations, people at full retirement age do not receive a full SSDI payment and a separate full retirement payment simultaneously on the same work record.

Instead, SSDI and retirement benefits are closely connected because both programs are generally based on a worker’s Social Security earnings history.

When a person receiving SSDI reaches Full Retirement Age (FRA), SSA generally converts SSDI benefits into retirement benefits automatically.

The monthly payment amount often remains similar, but the category of benefits changes from disability benefits to retirement benefits.

According to SSA rules, this conversion usually happens automatically at Full Retirement Age.

How Early Retirement and SSDI Can Interact

Some people apply for reduced early retirement benefits while an SSDI application is still pending.

This situation often happens when:

A worker can no longer continue working because of a medical condition,

They are close to retirement age, and

They need income while waiting for an SSDI decision.

Under SSA rules, a person may be allowed to apply for both early retirement and SSDI at the same time.

However, the programs work differently:

Early retirement is age-based.

SSDI is disability-based.

Early retirement benefits may be reduced if started before Full Retirement Age.

SSDI benefits are generally not reduced for age in the same way.

Early retirement and SSDI -Hierarchy and Interaction

In many situations, SSA may treat SSDI as the higher-paying disability-based benefit when a person qualifies medically.

If someone begins reduced early retirement benefits and is later approved for SSDI, SSA may adjust the payment structure and potentially pay disability benefits dating back to the established onset period, subject to SSA rules and waiting periods.

In some situations:

The person may temporarily receive reduced retirement payments while waiting for an SSDI decision.

SSDI approval may later replace some or all of the reduced retirement structure.

Once the person reaches Full Retirement Age, SSDI generally converts into retirement benefits automatically.

The rules governing these adjustments are primarily found in Title II of the Social Security Act, 20 CFR Part 404, and SSA’s internal Program Operations Manual System (POMS). Readers researching how SSA handles reduced early retirement benefits and later SSDI approval often review 20 CFR § 404.408, which addresses reductions when disability benefits become payable after reduced retirement benefits have already started. SSA also publishes internal POMS guidance involving recomputation, disability freezes, and conversion between Retirement Insurance Benefits (RIB) and Disability Insurance Benefits (DIB). (You can find links to regulations below in the References section.)

Because timing rules, offsets, retroactive benefits, and filing strategies can vary significantly, many applicants contact SSA directly or consult a licensed disability professional for guidance specific to their circumstances.

Why This Confuses So Many Applicants

Many people believe:

“Retirement and SSDI are completely separate checks.”

“Taking early retirement automatically prevents SSDI.”

“You cannot file for both.”

In reality, SSA rules can allow overlap and transitions between programs, especially for workers approaching retirement age who develop serious medical conditions.

Understanding the distinction between “retirement benefits,” “SSDI,” and simply “getting SSA” can help applicants make more informed decisions when starting the disability process.

Can Someone Receive SSI and Retirement Benefits Together?

In some cases, yes.

A person may receive both SSI and Social Security retirement benefits if:

Their retirement benefit amount is relatively low, and

They still meet SSI financial eligibility rules.

However, retirement income generally counts when SSA evaluates SSI eligibility and payment amounts.

That means retirement benefits may reduce SSI payments or make a person financially ineligible for SSI depending on income and resource levels.

Can Someone Receive SSDI and SSI Together?

Yes. Some individuals receive concurrent benefits, meaning they qualify for both SSDI and SSI at the same time.

This sometimes happens when:

A worker qualifies medically for SSDI,

Their SSDI payment is relatively low, and

They also meet SSI financial eligibility requirements.

SSA statistical reports track beneficiaries receiving concurrent benefits through multiple Social Security programs.

Because concurrent eligibility rules can become complex, many applicants choose to contact SSA directly or consult a licensed disability professional regarding their specific circumstances.

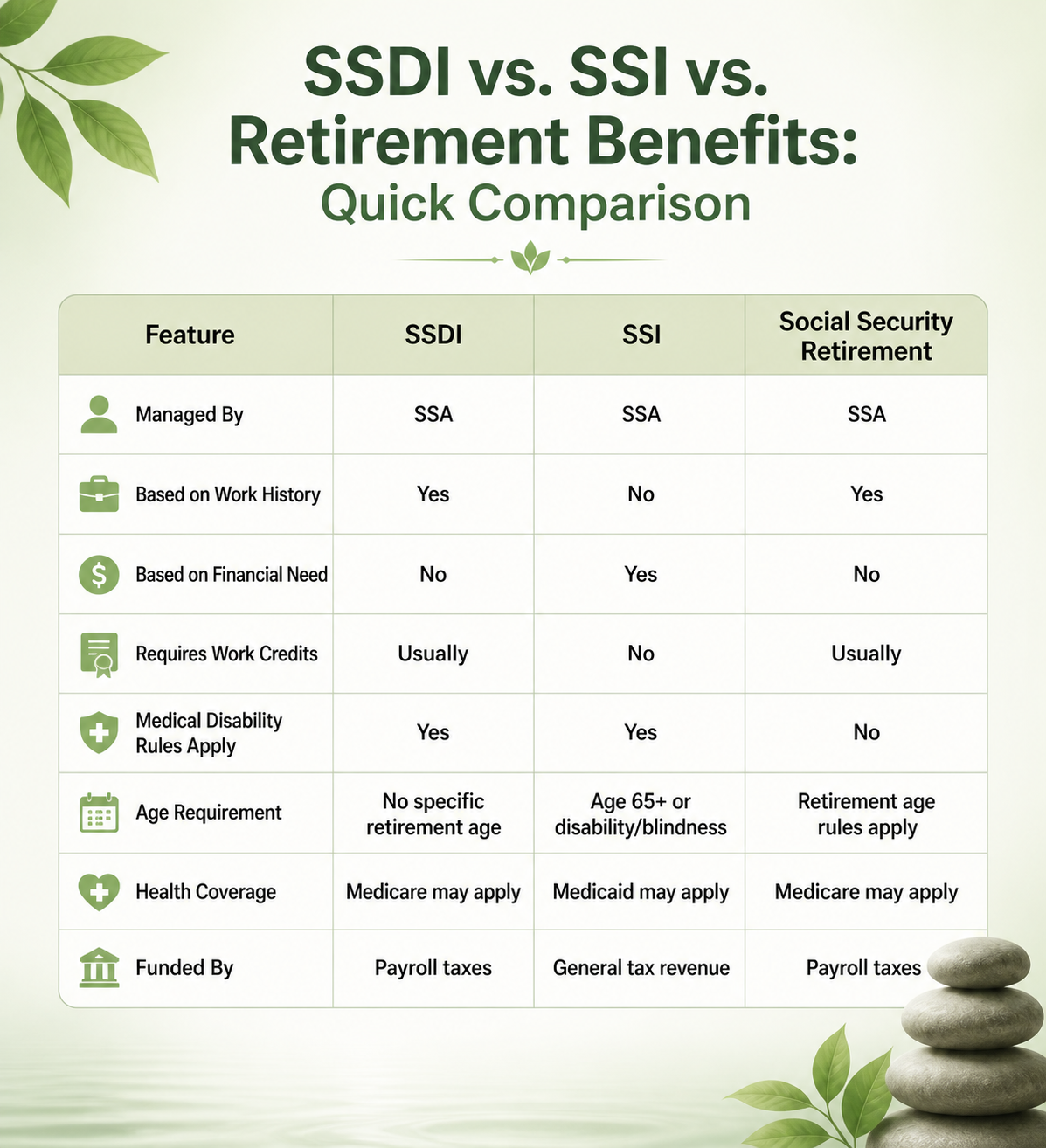

SSDI vs. SSI vs. Retirement Benefits: Quick Comparison

Table comparing the basic differences between SSDI, SSI, and Retirement through the U.S. Social Security Administration to help gain an understanding of the different government programs.

Common Misunderstandings About SSA, SSDI, SSI, and Retirement Benefits

“SSA Is a Benefit”

SSA is the agency, not the payment program.

“SSI and SSDI Are the Same”

Although they use similar disability rules, financial and work-history requirements are very different.

“Retirement Benefits and SSDI Always Stack Together”

In many cases, SSDI converts into retirement benefits at Full Retirement Age rather than continuing as a separate disability payment.

“Only Older Adults Qualify for Disability Benefits”

Younger adults and children can sometimes qualify for SSDI or SSI if eligibility requirements are met.

Summary

SSA, SSDI, SSI, and Social Security retirement benefits all sound similar, but they serve different purposes within the federal benefits system.

SSA is the agency that administers the programs.

SSDI is disability insurance tied to work history.

SSI is a financial-needs-based assistance program.

Retirement benefits are age-based payments tied to prior work contributions.

Some people may qualify for more than one program at the same time, while others may transition from SSDI into retirement benefits once they reach Full Retirement Age.

Understanding these differences can make the process feel less intimidating and help applicants know which programs may apply to their circumstances. Whether someone is beginning a Start disability application or helping a family member research benefits, learning the language of Social Security programs is often an important first step. You always reach out to a disability advocate or disability attorney to help guide you through the process.

FAQ

Q. Can a person receive SSDI and retirement benefits at the same time?

A. In some situations, a person may receive reduced Social Security retirement benefits while an SSDI application is pending. However, SSDI and retirement benefits are closely connected because both are generally based on the same Social Security earnings record. According to SSA guidelines, SSDI benefits usually convert automatically into retirement benefits once a person reaches Full Retirement Age (FRA).

Q. Can retirement income affect SSI eligibility?

A. Yes. Because SSI is a needs-based program, Social Security retirement income may affect eligibility or reduce monthly SSI payments.

Q. What does SSA stand for?

A. SSA stands for the Social Security Administration, the federal agency that manages SSDI, SSI, retirement benefits, and related Social Security programs.

References

Social Security Administration. (n.d.). Social Security Disability Insurance (SSDI) benefits. Retrieved from https://www.ssa.gov/disability

Social Security Administration. (n.d.). Retirement benefits. Retrieved from https://www.ssa.gov/retirement

Social Security Administration. (n.d.). Supplemental Security Income (SSI). Retrieved from https://www.ssa.gov/ssi

Social Security Administration. (n.d.). SSI eligibility requirements. Retrieved from https://www.ssa.gov/ssi/text-eligibility-ussi.htm

Social Security Administration. (n.d.). The Red Book: What’s New in 2026? Retrieved from https://www.ssa.gov/redbook/newfor2026.htm

Social Security Administration. (n.d.). Social Security Act: Title II—Federal Old-Age, Survivors, and Disability Insurance Benefits. Retrieved from https://www.ssa.gov/OP_Home/ssact/title02/0200.htm

Social Security Administration. (n.d.). Social Security Act: Title XVI—Supplemental Security Income for the Aged, Blind, and Disabled. Retrieved from https://www.ssa.gov/OP_Home/ssact/title16b/1600.htm

Social Security Administration. (n.d.). 20 CFR Part 404—Federal Old-Age, Survivors and Disability Insurance. Retrieved from https://www.ssa.gov/OP_Home/cfr20/404/404-0000.htm

Social Security Administration. (n.d.). 20 CFR Part 404, Subpart P—Determining Disability and Blindness. Retrieved from https://www.ssa.gov/OP_Home/cfr20/404/404-1501.htm

Social Security Administration. (n.d.). 20 CFR Part 404, Subpart P, Appendix 1—Listing of Impairments. Retrieved from https://www.ssa.gov/OP_Home/cfr20/404/404-app-p01.htm

Electronic Code of Federal Regulations. (n.d.). 20 CFR Part 404, Subpart P—Determining Disability and Blindness. Retrieved from https://www.ecfr.gov/current/title-20/chapter-III/part-404/subpart-P

Social Security Administration. (n.d.). 20 CFR Part 404, Subpart P, Appendix 2—Medical-Vocational Guidelines. Retrieved from https://www.ssa.gov/OP_Home/cfr20/404/404-app-p02.htm

Social Security Administration. (n.d.). 20 CFR § 404.408—Reduction where disability insurance benefits are payable after reduced old-age insurance benefits. Retrieved from https://www.ssa.gov/OP_Home/cfr20/404/404-0408.htm

Social Security Administration. (n.d.). 20 CFR Part 416—Supplemental Security Income for the Aged, Blind, and Disabled. Retrieved from https://www.ssa.gov/OP_Home/cfr20/416/416-0000.htm

Social Security Administration. (n.d.). 20 CFR § 416.1100—Income and SSI eligibility. Retrieved from https://www.ssa.gov/OP_Home/cfr20/416/416-1100.htm

Social Security Administration. (n.d.). 20 CFR § 416.1201—Resources and SSI eligibility. Retrieved from https://www.ssa.gov/OP_Home/cfr20/416/416-1201.htm

Centers for Medicare & Medicaid Services. (n.d.). Get started with Medicare: Eligibility and enrollment information. Retrieved from https://www.medicare.gov/basics/get-started-with-medicare

Social Security Administration. (n.d.). Medicare information for people with disabilities. Retrieved from https://www.ssa.gov/disabilityresearch/wi/medicare.htm

Social Security Administration. (2025). Annual Statistical Supplement, 2025. Retrieved from https://www.ssa.gov/policy/docs/statcomps/supplement/2025/

Disclaimer & AI Ethical Statement

Disclaimer: This article is for informational purposes only and does not constitute medical or legal advice. Consult with a qualified healthcare provider for any medical concerns or questions. Consult with a licensed attorney for legal advice.

AI Ethical Statement: This article includes information sourced from government and reputable health websites, reputable academic journals, non-profit organizations, and generated with help from AI. A human author has substantially edited, arranged, and reviewed all content, exercising creative control over the final output. People and machines make mistakes. Please contact us if you see a correction that needs to be made.